by Legalnaija | Jul 8, 2026 | Blawg

Over the years, I have unsuccessfully litigated the harmonisation of public databases in Nigeria. A fallout of this is the pending appeal Number CA/ABJ/CV/1460/2025 between Digital Rights Lawyers Initiative and Nigerian Interbank Settlement Systems Plc (NIBSS) on whether the NIBSS is statutorily empowered to manage a database of biometric data of Nigerian citizens, as opposed to NIMC, as well as the issue of privacy.

Hence, when news filtered that the President had assented to the National Identity Management Commission (NIMC) Act 2026 on Friday, 26 June 2026, I was curious about its implications for inter-agency (personal) data governance. After reading a copy of the bill, here are my brief thoughts on the freshly minted piece of legislation from a data protection perspective:

Worthy Reference to Data Protection

Remarkably, section 24(1) requires the NIMC to comply with the Nigeria Data Protection Act, 2023, and data protection best practices in operating the database. The section restricts the use of personal data to the specific purpose for which it was disclosed consistent with purpose limitation principles. The section, however, makes consent the primary gateway for disclosure while emphasising its revocability.

Section 18(8) reinforces the transparency principle by requiring NIMC to inform individuals at the point of registration about how their information will be used, who it will be shared with, and how they can exercise access rights. Keeping up with data minimisation requirements, section 20 limits what an identity document may display, restricting it to the NIN, date of birth, gender, citizenship status, and security feature. Section 25(3) expressly prohibits the Commission from retaining data on the purpose of authentication requests received from third parties in respect of a registrable person. This provision essentially curtails systemic surveillance measures. Interestingly, section 24(7) imposes a duty on anyone who uses or discloses database information to implement appropriate technical and organisational measures.

Data Harmonization

Of particular significance is the provision of section 7(c) to the effect that: “The Commission shall ….serve as the repository of all biometric data capture for the management of identity in the country for proper coordination and harmonisation”. By this provision, NIMC has been effectively designated as the exclusive national custodian of all biometric data gathered for identity management, with the duty to collate, update, and protect that data in a centralised repository. This role is expressly intended to promote proper coordination among all identity-issuing and identity-using agencies, ensuring that their systems align with common frameworks and exchange information efficiently. Ultimately, the Commission shall drive the harmonisation of identity management practices across the country, reducing redundancy, enhancing security, and enabling consistent service delivery for all individuals.

In similar terms, section 8(b) empowers NIMC to “harmonise and integrate the existing identification databases in government agencies and integrate them into the National Identity Database.” Beyond its repository function, this provision further empowers NIMC to undertake the active harmonisation and technical integration of all existing identification databases currently operated by various government agencies, departments, and parastatals. This entails a systematic process of data mapping, de-duplication, record linkage, and alignment to resolve inconsistencies, eliminate redundant entries, and establish a common semantic framework across disparate legacy systems. The ultimate objective is to seamlessly incorporate these agency-specific databases into the National Identity Database, thereby transforming a fragmented collection of siloed registers into a unified, interoperable, and authoritative identity infrastructure that supports secure authentication, efficient service delivery, and evidence-based policymaking across all tiers of government.

Conclusively, the NIMC Act 2026 arrives at a critical juncture in Nigeria’s evolving data governance landscape, and for those of us who have navigated the judicial trenches in pursuit of database harmonisation and privacy protection, it represents both a legislative triumph and a sobering reminder of the work that remains undone. My personal experience litigating the harmonisation of public databases, culminating in the pending appeal in Digital Rights Lawyers Initiative v. NIBSS (supra) has laid bare the institutional rivalries, legal ambiguities, and systemic inertia that have long frustrated efforts to establish a coherent identity management framework.

By designating NIMC as the exclusive repository for all biometric data and mandating the harmonisation and integration of existing government databases, the Act offers a progressively statutory answer to the core question in that appeal. However, I believe legislative clarity, though commendable, does not automatically translate into institutional compliance, unless all stakeholders proactively play their respective roles towards actualising the objectives of the new Act.

by Legalnaija | Jul 3, 2026 | Blawg

The British Nigeria Law Forum (BNLF) Nigeria Summit 2026 was held on 26th June 2026 under the theme “A New Dawn in Law, Investment and Opportunity in UK-Nigeria Relations.” The Summit commemorated the Forum’s 25th anniversary and convened lawyers, policymakers, business leaders, investors, regulators and professionals from Nigeria and the United Kingdom to discuss strengthening bilateral trade, investment and legal collaboration. The summit featured a Welcome address, a keynote speech, goodwill messages, and five thematic panel sessions focused on tax reform and investment, dispute resolution, intellectual property, cross-border networking, and divestment.

Mr. Kash Balogun, the Chairman of the BNLF, described the Summit as a platform for transforming dialogue into meaningful collaboration. He observed that the relationship between both countries extends beyond historical and sentimental ties; it is commercial, strategic, and rich with untapped potentials. He emphasized that potential alone is insufficient; progress demands a shift from conversation to collaboration, from relationships to results, and from goodwill to actionable opportunity. Reflecting on the BNLF’s 25 years journey, he reiterated the Forum’s commitment to serving as a bridge between both jurisdictions while supporting the next generation of professionals.

Delivering the keynote address, Professor Konyin Ajayi, SAN, likened the BNLF to a bridge that connects people, ideas, businesses and opportunities. He observed that the future of UK–Nigeria relations depends on trust, institutional strength, certainty, collaboration and fair trade. He urged stakeholders to focus on building confidence, capacity, embrace opportunities, build fair trade and build ambition.

Representing the Governor of Lagos State, Lawal Pedro, SAN, the Attorney General and Commissioner for Justice Lagos State, reaffirmed the State’s commitment to becoming the leading investment destination in West Africa. He noted that recent UK–Nigeria trade and investment agreements have already produced measurable progress in sectors such as financial technology, pharmaceuticals, education and the creative economy. He emphasized that sustainable investment requires legal certainty, transparent regulation, enforceable contracts and effective dispute resolution.

The first panel session explored the theme “Investment Climate under the New Tax Laws- Opportunities for Investors”

The Speakers examined the impact of Nigeria’s new tax framework on investment and agreed that the reforms represent a significant step towards creating a more business-friendly tax environment but stressed that tax reform alone cannot attract sustainable investment.

Key recommendations from the session included:

- Improving taxpayer education

- Strengthening institutional credibility and policy consistency;

- Attracting more Foreign Direct Investment (FDI) rather than Foreign Portfolio Investment (FPI);

- Encouraging businesses to adopt corporate structures capable of attracting investment; and

- Addressing structural challenges such as infrastructure deficits, currency instability and the trust deficit.

The panel concluded that investor’s confidence ultimately depends on certainty, effective institutions and predictable government policies.

The second panel under the theme “Future-Proofing Dispute Resolution Minimizing Delays and Maximizing Impact” explored strategies for improving commercial dispute resolution and reducing delays.

Speakers highlighted Lagos’ growing reputation as a regional dispute resolution hub through institutions such as the Lagos Court of Arbitration, the Lagos Multi-Door Courthouse and the Commercial Court. They emphasized the need for faster enforcement of arbitral awards, improved judicial capacity and stronger legislative reforms to enhance Nigeria’s credibility in international commercial transactions. The discussion also underscored the importance of cross-border cooperation and effective enforcement mechanisms in protecting commercial interests.

The third panel under the theme “Exploring the Business of Creativity, Intellectual Property Law Changes and Capital Flows” focused on intellectual property as an economic asset capable of attracting investment.

Speakers encouraged creators to register and protect their intellectual property at the earliest opportunity, noting that ownership remains the foundation for commercialization and investment. The panel also highlighted the growing impact of artificial intelligence on copyright law and the need for legislative reforms to address emerging technological developments. Other recommendations included developing a credible intellectual property valuation framework, strengthening judicial expertise in IP disputes, promoting licensing over outright assignment of rights, and improving access to IP financing.

The fourth panel under the theme “Cross-Border Networking – The Relationship stories behind Global Opportunities” examined the role of professional relationships in creating global opportunities.

Speakers emphasized that meaningful networking is built on authenticity, consistency and mutual value rather than transactional engagement. Participants were encouraged to communicate the value they offer, remain accessible, volunteer within professional communities and cultivate long-term relationships capable of generating future opportunities. The session reinforced the importance of trust and credibility as essential components of successful cross-border professional practice.

The final panel under the theme “Beyond Exit: What Divestment Means for Investment and Growth” considered the implications of divestment across key sectors of the Nigerian economy.

Speakers observed that corporate divestment should not necessarily be viewed negatively but rather as an opportunity for indigenous participation and increased domestic investment. Real estate, infrastructure and special economic zones were identified as sectors with significant investment potential. The panel also stressed the need for transparent land administration, improved power infrastructure, digitalization of regulatory processes and long-term policy stability to attract sustained investment.

Conclusion

The BNLF Nigeria Summit 2026 reaffirmed the importance of strong legal institutions, strategic partnerships and predictable regulatory frameworks in advancing UK–Nigeria relations. As the Forum celebrates twenty-five years of fostering collaboration between both jurisdictions, the Summit demonstrated that sustainable investment and economic growth will depend on trust, innovation, effective governance and continued engagement between governments, legal practitioners, businesses and investors. Overall, the Summit provided practical insights and actionable recommendations capable of strengthening the legal and commercial relationship between Nigeria and the United Kingdom while positioning both countries for greater collaboration in the years ahead.

by Legalnaija | Jul 1, 2026 | Blawg

The United Kingdom offers various visa types for Nigerian citizens, each designed to fit specific purposes, from short visits to long-term stays for work, study, or family reunification. Knowing which visa to apply for is essential to ensure a smooth application process. This article covers the main types of UK visas available to Nigerians, along with eligibility requirements and application details.

The various types of UK visas for Nigerian nationals are as follows:

- UK Visitor Visas

- UK Work Visas

- UK Study Visas

- UK Family Visas

- UK Business Visas

- UK Transit Visa

- Settlement Visas and Indefinite Leave to Remain (ILR)

- UK Ancestry Visa

- UK Visitor Visas

These are for short stays (usually up to 6 months, though longer multiple-entry visas exist).

Common Visitor Visa Types

- Standard Visitor Visa-Tourism, visiting family/friends, short business trips.

- Marriage Visitor Visa-Visit the UK to get married/civil partnership

- Permitted Paid Engagement Visa-For expert paid short-term engagements.

www.legalnaija.com/store

- Work Visas

These are for Nigerians who have a job offer from a UK employer with a valid sponsor license.

Main Work Visa Routes

- Skilled Worker Visa-For skilled professionals with a job offer that meets skill/salary thresholds.

- Health and Care Worker Visa-For medical and care professionals working in the NHS or approved care roles.

- Global Business Mobility Visas-Senior/specialist or expansion worker categories.

- Temporary Work Visas-Seasonal Worker, Charity Worker, Creative Worker, Religious Worker, etc.

- High Potential Individual-For high-potential graduates and scale-up roles

- Study Visas

For Nigerians planning to study in the UK:

- Student Visa (formerly Tier 4)-For university, college, or other full-time studies. Requires a Confirmation of Acceptance for Studies (CAS) from a licensed UK institution.

- Short-term Study Visa-For short courses (e.g. English language courses or other brief programs).

- Family Visas

For Nigerians joining family members in the UK or planning to settle.

- Spouse/Partnership Visa-Join a spouse or partner who is a UK citizen or settled in the UK.

- Fiance/Proposed Civil Partner Visa-To come and marry in the UK.

- Unmarried Partner Visa-For long-term partners.

- Adult Dependent Relative Visa-For relatives who need care for a UK-based family member.

- Child Dependent Visa-For children of UK citizens/settled persons.

5.UK Business Visas

The UK offers several visas for Nigerian entrepreneurs and investors looking to start or invest in businesses:

- Innovator Visa: For experienced entrepreneurs with innovative business ideas. This visa requires a minimum investment of 50,000 GBP and endorsement from a recognized UK body

- Start-Up Visa: For new entrepreneurs with an innovative business idea endorsed by an approved UK institution. Unlike the Innovator Visa, this visa does not require an initial investment but is valid for only two years, after which applicants may switch to an Innovator Visa.

- Investor Visa: For high-net worth individuals investing at least 2 million GBP in the UK. The visa is initially valid for three years and four months, with the option to extend.

Business visas are suitable for Nigerians who wish to establish or expand businesses in the UK, providing pathways to permanent residency for successful entrepreneurs and investors.

- Transit Visas

The Transit Visa is for Nigerians who are traveling through the UK to reach another destination. It allows you to pass through the UK airport without leaving the airport’s transit area.

- Direct Airside Transit Visa (DATV): This type of transit visa enables travelers to pass through a UK airport without entering the UK border area.

- Visitor in Transit Visa: For stopping in the UK en route to another country.

- Settlement Visas and Indefinite Leave to Remain (ILR)

Settlement visas and Indefinite Leave to Remain (ILR) are for Nigerians who wish to settle permanently in the UK. Common pathways include:

- Spouse or Partner Visa Route: After five years in the UK on a Spouse or Partner Visa, applicants can apply for ILR.

- Skilled Worker Visa Route: Skilled Worker Visa holders can apply for ILR after five years of continuous residence in the UK.

- Ancestry Visa Route: Nigerians with a UK-born grandparent can qualify for a UK Ancestry Visa, allowing them to work and live in the UK for five years, with the option to apply for ILR after this period.

- Ancestry Visa

The UK Ancestry Visa is available to Nigerians who have a UK-born grandparent and wish to live and work in the UK.

Eligibility Requirements

- UK-Born Grandparent: Proof of the grandparent’s birth in the UK.

- Intent to work: Applicants must plan to work or seek work in the UK.

The Ancestry Visa is valid for five years and can lead to permanent residency.

Conclusion

As previously stated, the UK has different types of visas. Each visa serves a different purpose. Nigerian nationals should seek the advice of a UK Immigration lawyer or a Nigerian based lawyer who’s licensed to practice in the UK.

by Legalnaija | Jun 29, 2026 | Blawg

The air at the cocktail was electric. Industry titans, dealmakers, clergy, and captains of commerce gathered not merely to witness a transition but to affirm something they had long known. Perchstone & Graeys, one of Nigeria’s most consequential commercial law firms, had entered a new chapter.

The occasion was the formal announcement of Dr Tolu Aderemi as the new Managing Partner of the 29-year-old firm, a moment that blended nostalgia with unmistakable forward energy.

Uyi Akpata, Regional Director of PwC Africa, opened the conversation on sustainability and succession planning, setting the intellectual tone for an evening that would prove far more than ceremonial. His remarks landed with particular weight in a room full of people who had built things and understood what it costs to keep them standing.

The founders, Remi Okunlola and Osaro Eghobamien SAN, then took the room on a journey through 29 years of building. They spoke of wins and losses, of opportunities seized and some missed, but above all, of the three things that kept the firm alive and respected through every season: character, integrity, and hard work. There was nothing rehearsed about it. The room listened.

Dr Ibukun Awosika, former Chairman of First Bank of Nigeria Plc, brought her characteristic clarity to the evening. She spoke on the imperative of doing business with integrity and sustainability, and commended Perchstone & Graeys as a firm she had watched distinguish itself over the years through exactly those values. Her words carried the authority of someone who does not give praise lightly.

Then came the moment the evening had been building toward.

Osaro Eghobamien, who had served as Managing Partner for over two decades and who had personally navigated the firm through some of Nigeria’s most defining commercial moments, formally announced Dr Tolu Aderemi as his successor. It was emotional. It was confident. And it was clear that this was not a handover born of fatigue but one born of faith.

Dr Aderemi rose to the occasion with the composure of someone who had long been in the room and was now simply standing at its centre. He paid tribute to the founders without sentimentality, acknowledging that what the firm enjoys today was built by people who had the discipline to build it right.

He then offered the room a frame for understanding what Perchstone & Graeys has always been and what it intends to remain. He called it the theory of the room. At every defining moment in Nigeria’s commercial history, whether the banking reforms, the recapitalisation of 2004, the oil boom between 2005 and 2008, or the major transactions that reshaped entire sectors, Perchstone was either in the room or building the room. That, he said, is not coincidence. It is character expressed commercially.

Looking forward, Dr Aderemi was precise. The firm will operate on three pillars: integrity, business acumen, and ingenuity. These are not aspirational words. They are the operating architecture of how Perchstone will serve its clients and conduct its internal affairs going forward.

He also announced a decisive shift in service delivery. All client instructions will now be subjected to technology, with artificial intelligence and blockchain, including the tokenisation of assets, forming part of how the firm works. This is not a firm chasing trends. This is a firm that has always understood where things are going before others arrive there.

The highlight of the evening was the unveiling of a new logo for Perchstone & Graeys, followed by the official decoration of the firm’s partners with the new insignia. It was a visual declaration. Something had changed. Something had also remained exactly the same.

Dr Stella Okoli OON, Chairman of Emzor Pharmaceuticals, added her voice to the evening, praising the firm for building a structure that can sustain itself and grow beyond its founders. That, in a country where institutional memory often walks out with the people who created it, is no small thing.

The guest list itself told a story. Austin Avuru, founder of Seplat and now Chairman of AA Holdings, was present. So was Pa Wigwe, father of the late Herbert Wigwe, former CEO of Access Bank. The Anyaim Osigwe brothers were in the room. The leadership of the Chartered Institute of Bankers of Nigeria attended. Representation came from oil and gas, power, renewable energy, banking and finance, and the clergy. Nigeria’s business community did not send delegates. It showed up.

Perchstone & Graeys turns 29 having buried nothing and abandoned nothing. Under Dr Tolu Aderemi, it carries its history as an asset and its future as a commitment. For anyone doing serious business in Nigeria, that is a firm worth knowing.

by Legalnaija | Jun 18, 2026 | Blawg

Beyond the Ballot Box: Why Voters’ Privacy Will Define Trust in Nigeria’s 2027 Election

As Nigeria prepares for the 2027 General Elections, public discourse has understandably focused on electoral credibility, transparency, security, logistics, and the ability of institutions to deliver a free and fair election. However, one issue that demands equal attention is the protection of voters’ personal data and its impact on public trust. In today’s digital age, elections are no longer driven solely by physical processes. From voter registration and biometric identification to digital databases and electronic communication platforms, technology has become deeply embedded in electoral administration. While these innovations provide opportunities for greater efficiency and transparency, they also create significant risks if personal information collected from citizens is not adequately protected.

The question before Nigeria ahead of 2027 is therefore not only whether citizens can exercise their right to vote freely, but also whether they can trust that the personal information they rovide as part of the electoral process will be handled responsibly, securely, and lawfully. It is against this backdrop that the Digital Rights Lawyers Initiative (DRLI) will convene a national conversation titled “2027 General Elections, Voters’ Privacy and Public Trust: Matters Arising” on Wednesday, 24 June 2026. The event will provide a platform for stakeholders across Nigeria’s electoral and digital rights ecosystem to examine the challenges, opportunities, and responsibilities associated with protecting voters’ personal information ahead of the next general elections.

The virtual convening will bring together key industry experts. It will feature leading voices in human rights, accountability, and digital governance, including Kolawole Oluwadare, Deputy Director of the Socio-Economic Rights and Accountability Project (SERAP); Khadijah El-Usman, Senior Programs Officer at Paradigm Initiative; Inibehe Effiong, Principal of Inibehe Effiong Chambers; and the Head of Research and Monitoring & Evaluation at Yiaga Africa. The conversation will be moderated by Solomon Okedara, Co-Founder of DRLI.

Speaking on the importance of the convening, Solomon Okedara, Co-Founder of DRLI, stressed that voters’ privacy must become a central component of Nigeria’s electoral preparedness.

“Public trust in elections is not built only at polling stations. It is also built through confidence that citizens’ personal information is collected, processed, and protected responsibly. When citizens provide their data to institutions, they must have assurance that such information will not be exposed, exploited, or used in ways that undermine their rights.”

Okedara also highlighted the enormous responsibility placed on INEC as one of Nigeria’s largest data controllers.

“INEC is one of the largest data controllers in Nigeria, processing the personal information of over 93 million registered voters. The scale and sensitivity of this data create significant responsibilities and risks. Any compromise of electoral data could have consequences beyond individual privacy; it could affect public confidence in the credibility of the electoral process.”

The concerns surrounding electoral data protection extend beyond cybersecurity. They raise important questions about accountability, transparency, oversight, and institutional responsibility. As Nigeria continues to adopt technology-driven approaches to electoral management, there must be clear safeguards to ensure that digital transformation strengthens democracy rather than creates new vulnerabilities. As Nigeria approaches another significant electoral milestone, one message is clear, the integrity of the 2027 General Elections will depend not only on the ballot cast by millions of Nigerians but also on the protection of the personal information that enables their participation.

The programme is proudly supported by Luminate, whose partnership with DRLI reflects a shared commitment to advancing digital rights, strengthening democratic accountability, and promoting responsible technology governance in Nigeria.

by Legalnaija | Jun 5, 2026 | Blawg

He Claimed He Deserved a Second Class Upper Degree, but His University Insisted on a Second Class Lower. So, Who Was Right? The Case Of Victor v. F.U.T.A. (2026) 8 NWLR (Pt. 2044) 33.

It is said that every case tells a story, but this case did not merely tell a story; rather, it engraved courage and demonstrated that one should be unflinchingly audacious in the pursuit of a legitimate claim. The facts concern something many students can easily relate to: examination results, and the hero in this judicial drama is a layman named Mr. Adebayo A. Victor, who remained extremely adamant for years in pursuit of getting the Second Class Lower Division grade awarded to him by his university upgraded to a Second Class Upper Division, which he believed was what he truly merited.

Interestingly, throughout these years, this layman pursued the case by himself all the way to the Supreme Court. This is indeed something to marvel at.

Nota bene, when we say “layman” in legal profession, we simply mean a person who is not a legal practitioner. No disrespect whatsoever is intended. Rather, the expression is used to emphasize the ingenuity, determination, and resilience of Victor who, despite not being a lawyer, pursued the case personally from the Federal High Court up to the Supreme Court. That being said, let us now properly dwell on the surrounding circumstances that midwifed this case.

Victor was the cross-appellant in this appeal. The Federal University of Technology, Akure (FUTA) was the 1st cross-respondent, while its Registrar, by virtue of his office, was also made a party as the 2nd cross-respondent. He (Victor) was a student of Mechanical Engineering at FUTA. In 2007, he graduated and was awarded a Second Class Lower Division degree. However, he was dissatisfied and was convinced that the degree classification awarded to him did not reflect his actual academic performance. According to him, some of his examination scores were incorrectly recorded. Consequently, he applied for the remarking of several courses, namely: MEE 202, MEE 301, MEE 302, MEE 305, MEE 307, MEE 308, MEE 309, MEE 311, MEE 312, and MEE 352.

Why was he so persistent?

Because he believed that if those scripts were properly re-marked, he would emerge not as a Second Class Lower graduate but as a Second Class Upper graduate. For about four years, from 2007 to 2011, he tried to exhaust every available avenue within the university system. Unfortunately, the university refused to yield to his request for the remarking.

At that point, Victor did what many students would probably never contemplate doing. He approached the Federal High Court, Lagos Division, in August 2011 seeking several reliefs, including orders directing the university to remark his scripts through independent assessors, issue his correct transcript and certificate, and compensate him for the losses he had suffered.

I believe many of us would just take fate and would never think of taking the above bold step, or do you believe you have Victor’s courage and could do the same? Anyway, hold the answer to yourself.

When the matter came up for hearing at the Federal High Court, it was dismissed on 16 January 2013 on the ground that it was statute-barred.

The university would, of course, be naturally satisfied, while Victor was not and did not believe that was the end, as many litigants would do. He appealed. And certainly, the Court of Appeal reasoned with Victor that his case was not statute-barred. Consequently, on 29 November 2013, the court set aside the decision of the trial court and ordered a retrial.

Looks like Victor had won the first round, right?

Indeed, he had. Now they were back to square one at the trial court.

Fresh pleadings were filed, issues were joined, and the matter proceeded to full trial. At the conclusion of the trial, the Federal High Court delivered judgment on 28 September 2017. The court found substantially in favour of Victor, though not on all his reliefs. Specifically, the court granted reliefs 5 and 7. The first was an order directing the cross-respondents to remark Victor’s examination scripts through external examiners. The second was an order directing the respondents to issue a final result and transcript reflecting his actual performance in the examinations. The court further awarded the sum of ₦500,000 (Five Hundred Thousand Naira) as general damages in favour of Victor. Victor had won. The university had lost. Naturally, one would expect the university to simply comply and move on.

It did not. The university refused to obey the orders immediately. Instead, dissatisfied with the judgment, it appealed to the Court of Appeal.

Victor too was not entirely happy.

He was like, after all these years, after all the stress, after all the emotional torture, after losing opportunities, after being denied the benefit of his actual academic standing, is this really what I am taking home? Surely this cannot be all.

And think about it. According to Victor, he had lost the opportunity of benefiting from the Nigeria Agip Exploration 2010/2011 International Postgraduate Scholarship Award, a fully funded Master’s programme in the United Kingdom. He had suffered emotional distress, repeated travels, financial hardship, and several years of uncertainty. So, I do not blame him at all.Consequently, he filed a cross-appeal.

For those unfamiliar with the concept, a cross-appeal is simply an appeal filed by a party who won the case but is nevertheless dissatisfied with some aspect of the judgment. Such a party is called a cross-appellant. In other words, both parties were unhappy, albeit for different reasons.

At the Court of Appeal, Lagos Division, one of the major issues concerned several documents that had been rejected by the trial court. The Court of Appeal held that Exhibits A, B, E, and O were private documents and not public documents as the trial court had held. Therefore, they did not require certification before being admitted in evidence.

The court also frowned at the conduct of the university in withholding documents after being served with a notice to produce. According to the court, a party cannot sit on documents, refuse to produce them, and later turn around to complain that the opposing party failed to prove facts contained in those very documents.

That would certainly be unfair, wouldn’t it? After all, that conduct of the University is not in due fidelity to the expectations of the provisions of the evidence Act specifically section 167 of the Evidence Act, as Indeed, “Justice is not a fencing game where one party seeks to outsmart the other.” ~Per Ogunwumiju JSC

Eventually, the Court of Appeal dismissed the university’s appeal in its entirety. Victor’s cross-appeal succeeded only in part. The court awarded him ₦50,000 (Fifty thousand) as costs at the trial court and ₦200,000(Two hundred thousand) as costs of the cross-appeal.

The university was unhappy.

Victor was equally unhappy.

Looks like both parties had become regular customers of the appellate courts, right?

And so they both found their way to the Supreme Court. However, before the hearing of the appeal, the university had a change of heart. Following the intervention of the Supreme Court, the university withdrew its appeal, which was subsequently dismissed on 21 June 2022.

Why did the university withdraw?

The answer is not far-fetched.

By then, the university had eventually complied with the orders directing the remarking of Victor’s scripts.

And guess what?

Victor was right.

The remarking exercise upgraded his degree classification from Second Class Lower Division to Second Class Upper Division.

The university subsequently issued his transcript and degree certificate accordingly. In fact, during one of the subsequent proceedings before the Supreme Court, Victor’s certificate and transcript were physically handed over to him in open court.

The university also informed the court that it had paid the earlier awards of ₦500,000 (Five hundred thousand) damages and ₦250,000 (Two-fifty) costs.

What then remained?

Of course, Victor’s cross-appeal challenging the inadequacy of the damages and costs awarded by the lower courts. He therefore urged the Supreme Court to award substantially higher compensation considering the years of hardship, emotional distress, lost opportunities, and frustration he had endured.

The appeal eventually came before a panel of five eminent Justices of the Supreme Court, namely John Inyang Okoro, JSC, who presided; Helen Moronkeji Ogunwumiju, JSC, who delivered the lead judgment; Obande Festus Ogbuinya, JSC; Stephen Jonah Adah, JSC; and Abubakar Sadiq Umar, JSC.

Supreme Court per Ogunwumiju, JSC, in unraveling the wool beclouding the judicial posers made reference to several authorities and lucidly explained that universities possess the exclusive authority to award degrees and determine academic standards. Courts generally do not interfere with academic judgments.

However, does that mean a university can act however it pleases?

The answer is in the negative. A university owes a duty of care to its students. For years, Victor persistently complained about his results and requested a review. Yet the university refused to investigate the complaint or re-mark the scripts until compelled by court orders.

It is the view of the Supreme Court that, that conduct amounted to a breach of the duty of care owed to Victor as its student.

The Court Per Ogunwumiju, further emphasized again that though academic decisions are generally not subject to judicial interference, where there is evidence of negligence, bias, procedural unfairness, or a breach of duty of care, the courts will not fold their arms. My Lord added, the duty of care owed by a university extends to academic, administrative, and welfare matters. A university must provide fair assessment procedures, competent supervision, transparent academic processes, proper handling of complaints, fair decision-making, and reasonable administrative support. My Lord reasoned that, in the instant case, the respondents abandoned that duty of care.

Supreme Court, then proceeded to explain the law relating to damages.

As we know, where a person successfully establishes a tortious wrong against another, he is generally entitled to general damages. Such damages flow naturally from the wrong and need not be specifically pleaded or strictly proved.

On the other hand, special damages, such as specific financial losses, medical expenses, or lost earnings, must be strictly proved.

The Court therefore agreed that, Victor had not sufficiently proved some of his claims for special damages, particularly the claim relating to lost earnings.

However, the Court held that there was no doubt that he suffered emotional distress, hardship, inconvenience, frustration, and loss of opportunities as a direct consequence of the university’s conduct.

The Court further observed that by 2017, when the trial court awarded ₦500,000 as general damages, Victor had already endured approximately ten years of suffering. According to the Supreme Court, that amount was simply too small in the circumstances.

The award could not be merely symbolic; it had to be genuinely compensatory. Consequently, the Supreme Court reviewed the award upward.

And not by a small margin.

The sum of ₦500,000 (Five hundred thousand) awarded by the lower courts was set aside and replaced with ₦18,000,000 (Eighteen Million Naira) as general damages for breach of duty of care and the emotional and physical stress suffered by Victor.

Furthermore, the court awarded ₦2,000,000( Two Million Naira)as costs of litigation, recognizing that although Victor was a layman, he had personally prosecuted the matter through the entire hierarchy of courts and incurred substantial expenses in so doing. In effect, Victor left the litigation with two major victories.

First, he obtained the Second Class Upper Division degree he had been pursuing since 2007.

Second, he obtained a total monetary award of ₦20,000,000.(Twenty Million Naira).

Please pause for a moment and clap for Victor.

He truly deserves it.

Remember, this was not a lawyer. This was a man who personally prosecuted his case from the Federal High Court to the Court of Appeal and ultimately to the Supreme Court.

He challenged a university. He lost at the first stage. He appealed. He returned for a retrial. He won. He defended that victory through the Court of Appeal. He defended it again before the Supreme Court. And in the end, he was vindicated.

All the other Justices adopted the reasoning of Ogunwumiju, JSC, and abided by the award hook, line, and sinker, having disclosed not an atom ounce of hostility that could warrant their reprobation of the lead judgment.

Lastly, it is gleanable from the above legal anatomy that although universities possess academic autonomy and retain the exclusive right to award degrees, they must nevertheless act fairly in dealing with students. Certain class of degrees should not be awarded according to whims and caprices. Those who genuinely work for them should receive them, as students’ futures may depend on the decisions made by university authorities.

This decision therefore serves as a reminder that while courts may be reluctant to interfere in academic matters, they will not hesitate to intervene where a university abandons its duty of care and subjects a student to avoidable hardship.

And perhaps that is the greatest lesson from this case. I will say no more, believing I have passed the message.

_______________________________________________________________

Isah Bala Garba is a Level 400 student of Common and Islamic Law of Bayero University, Kano,(SABUK). He has authored numerous legal articles and analyzed many cases in clear, plain language. He can be reached for comments or corrections on: LinkedIn: https://www.linkedin.com/in/isah-bala-garba-301983276 isahbalagarba05@gmail.com or on 08100129131.

by Legalnaija | Jun 3, 2026 | Blawg

Elevate Your Brand: Sponsorship Opportunities for the BNLF Nigeria Summit 2026

In an increasingly interconnected global economy, the bridge between legal expertise and business strategy has never been more critical. We are thrilled to announce that the BNLF (British Nigeria Law Forum) Nigeria Summit 2026 is returning to Lagos, promising to be the premier gathering for legal and business professionals bridging the UK and Nigerian markets.

As we prepare for this milestone event, we are opening our doors for strategic partners who are ready to position their brand at the intersection of influence, innovation, and international collaboration.

Why Partner with the BNLF Nigeria Summit?

The BNLF Summit is more than just a conference; it is a catalyst for high-level professional engagement. By sponsoring this event, your organization gains direct access to:

• A High-Profile Audience: Engage with industry titans, legal experts, policymakers, and C-suite executives from both Nigeria and the UK.

• Brand Authority: Align your brand with the reputation of the BNLF, showcasing your commitment to excellence and cross-border collaboration.

• Strategic Connections: Move beyond traditional networking. The summit is designed to facilitate meaningful conversations that transform into long-term business partnerships.

• Market Visibility: Secure prominent placement throughout our marketing campaigns, event collateral, and the two-day experience in Lagos.

The Details*

• Location: Lagos, Nigeria

• Dates: June 25–26, 2026

Secure Your Place as a Partner

Opportunities for sponsorship are now live, but they are limited. We invite you to join us as we create a platform where influence meets opportunity.

Whether you are looking to launch a new initiative, reinforce your brand’s market leadership, or tap into the vibrant UK-Nigeria professional corridor, we have a sponsorship package tailored to your needs.

Ready to partner with us?

1. Register your interest here: https://tinyurl.com/BNLF26

2. Have questions? Reach out to our team directly at 09134619903 or 09095635314.

Don’t miss this chance to be a part of the most impactful professional gathering of 2026. Let’s build the future of collaboration together

#BNLFSummit2026 #SponsorshipOpportunity #BrandVisibility #Networking #LegalProfessionals #LagosEvents #BusinessGrowth

by Legalnaija | Jun 1, 2026 | Blawg

Building Cross-Border Legal Opportunities: Why Law Firms Should Join the BNLF 25th Anniversary Summit & Gala

As the legal community anticipates the upcoming British Nigeria Law Forum (BNLF) 25th Anniversary Summit & Gala, it’s worth reflecting on the remarkable success of last year’s BNLF Nigeria Summit 2025—a timely reminder of the power of cross-border collaboration.

Looking Back: The 2025 Summit in Lagos

Held under the theme “Strengthening Legal and Business Ties Between the UK and Nigeria: Navigating Opportunities and Challenges”, the 2025 Summit set a high bar for legal engagement. The event featured:

• Fireside chats on the power of legal networks with industry heavyweights.

• Debates on the integration of Artificial Intelligence and cryptocurrency into modern legal practice.

• Networking opportunities that fostered lasting cross-continental relationships.

Attendees walked away with deeper insights into accessing international markets and strategies for building a global legal brand—proof that the synergy between UK and Nigerian practitioners is stronger than ever. The connections made in Lagos have continued to generate conversations and opportunities across both countries.

The 2026 Milestone: A New Dawn

Building on that foundation, the BNLF Summit & Gala 2026 (June 25–26, Lagos) promises to be the most significant gathering yet. Anchored by the theme “A New Dawn in Law, Investment and Opportunity in UK–Nigeria Relations”, the summit will feature:

• Keynote addresses from distinguished figures such as Prof. Konyin Ajayi, SAN.

• High-level roundtable discussions chaired by Florence Eshalomi MP, UK Trade Envoy to Nigeria and Ghana.

• A grand Gala Dinner, celebrating 25 years of excellence in UK–Nigeria legal relations.

Why Law Firms Should Attend

For law firms, the Summit is more than an event—it’s a strategic opportunity to:

• Build cross-border relationships that lead to referrals, partnerships, and new business.

• Position your firm globally by engaging with thought leaders and policymakers.

• Stay ahead of trends in international law, investment, and emerging technologies.

The BNLF has consistently proven itself as the premier platform for fostering collaboration between UK and Nigerian legal communities. This 25th Anniversary Summit is set to amplify that impact.

Secure Your Place

Interest is building rapidly, and organizers are urging professionals to register early to ensure their place in these pivotal conversations.

Register for the 2026 BNLF Summit https://tinyurl.com/BNLF26

For sponsorship or event details, contact the BNLF at 09134619903 or 09095635314.

by Legalnaija | May 25, 2026 | Blawg

Meet Our Esteemed Speaker at the BNLF Summit, Conference & Gala Night 2026

The British Nigeria Law Forum (BNLF) is delighted to announce Dr. Mobolaji Ojibara, Ph.D., FNIM, FCIArb as one of our distinguished speakers for the BNLF Summit, Conference & Gala Night 2026.

Dr. Ojibara is a highly respected Nigerian legal practitioner, arbitrator, governance expert, and institutional administrator, with over two decades of exceptional experience spanning Corporate & Commercial Law, International Commercial Arbitration, Dispute Resolution, and Governance Advisory. He is also a proud Member of the Distinguished Body of Benchers in Nigeria, reflecting his outstanding contributions to the legal profession and institutional leadership.

As the British Nigeria Law Forum celebrates 25 years of fostering legal collaboration and strengthening professional ties between Nigeria and the United Kingdom, we are honored to welcome Dr. Ojibara to what promises to be a landmark gathering of legal minds, policymakers, business leaders, and industry professionals.

Join us on 25–26 June 2026 in Lagos, Nigeria, for two impactful days of insightful conversations, strategic networking, and meaningful discussions exploring the future of law, governance, investment, and cross-border opportunities between the UK and Nigeria.

Whether you are a legal practitioner, business executive, policymaker, or professional seeking to build valuable connections, this is an event you do not want to miss.

🎟️ Registration is now open: https://tinyurl.com/BNLF26

#BNLF25 #BNLFSummit2026 #BritishNigeriaLawForum #LegalLeadership #Governance #DisputeResolution #UKNigeriaRelations #ConferenceAndGalaNight

by Legalnaija | May 23, 2026 | Blawg

BNLF Announces Prof. Konyin Ajayi, SAN, as Keynote Speaker for its 25th Anniversary Nigeria Summit 2026

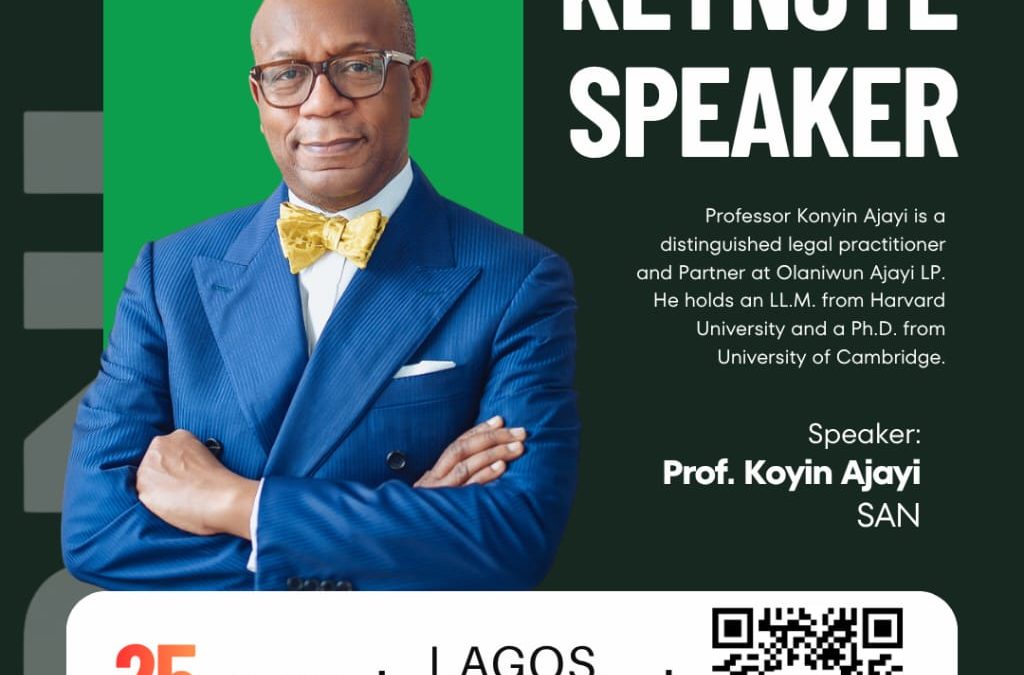

The legal and business communities across Nigeria and the United Kingdom are set for one of the most anticipated cross-border events of the year as the British Nigeria Law Forum (BNLF) officially announces Professor Konyin Ajayi, SAN, as the Keynote Speaker for the BNLF Nigeria Summit 2026 taking place in Lagos this June.

A distinguished legal practitioner and Partner at Olaniwun Ajayi LP, Prof. Konyin Ajayi, SAN, is widely respected for his contributions to legal practice, corporate governance, and dispute resolution. With an LL.M. from Harvard University and a Ph.D. from the University of Cambridge, his keynote address is expected to provide deep insights into the evolving legal, commercial, and investment relationship between the United Kingdom and Nigeria.

This year’s Summit is particularly significant as it marks the 25th Anniversary of the British Nigeria Law Forum — a milestone celebration of collaboration, professional excellence, and cross-border engagement between legal practitioners in both jurisdictions.

Under the theme:

“A New Dawn in Law, Investment and Opportunity in UK–Nigeria Relations”

the Summit will convene leading legal professionals, policymakers, regulators, investors, academics, and business executives to discuss emerging opportunities and pressing developments shaping the future of UK-Nigeria relations.

Event Details

Dates: June 25 – 26, 2026

Location: Lagos, Nigeria

What Participants Can Expect

June 25, 2026

The Summit will commence with exclusive invitation-only Roundtable Discussions chaired by Florence Eshalomi MP, UK Trade Envoy to Nigeria & Ghana. The sessions will bring together influential stakeholders to engage in high-level conversations around law, trade, investment, and bilateral partnerships.

The day will conclude with an elegant Cocktail Reception hosted at the Residence of the Deputy British High Commissioner in Lagos, providing attendees with premium networking opportunities in a distinguished setting.

June 26, 2026

The International Conference will feature insightful keynote addresses, expert-led masterclasses, and panel discussions focused on critical sectors and emerging legal trends, including:

Divestment and investment opportunities

Intellectual Property Law

New Tax Laws and regulatory reforms

Future-proofing dispute resolution mechanisms

Cross-border legal and commercial opportunities

The Summit will culminate in a prestigious Gala Dinner celebrating 25 years of impact, collaboration, and professional excellence.

Why You Should Attend

As cross-border dynamics continue to evolve, the BNLF Nigeria Summit 2026 presents a rare opportunity for legal practitioners, business leaders, investors, and policymakers to:

Build strategic international connections

Gain valuable industry insights

Explore investment and commercial opportunities

Engage directly with leading voices in law and business

Position themselves at the forefront of UK-Nigeria legal and economic relations

With a lineup of distinguished speakers and carefully curated sessions, this Summit promises to be both impactful and transformational.

Registration & Enquiries

Spaces are strictly limited, and early registration is strongly encouraged.

Register Here: tinyurl.com/BNLF26

Official Website: www.bnlf.org.uk

For enquiries and sponsorship opportunities, contact:

09134619903

09095635314

Info@bnlf.org.uk

The British Nigeria Law Forum invites members of the legal profession, corporate leaders, policymakers, and stakeholders across industries to be part of this landmark event as it celebrates 25 years of strengthening legal and commercial ties between Nigeria and the United Kingdom.